")

Judgment Update l Levy of IGST on ocean freight in case of CIF imports held unconstitutional

This is to apprise you on recent Gujarat High Court judgment in the case of Mohit Minerals Private Limited and Ors. v. UOI, 2020-VIL-36-GUJ wherein the High Court has held the levy of IGST on ocean freight charges (in case of CIF imports) as unconstitutional and ultra-vires the Integrated Goods and Services Tax Act, 2017 (‘IGST Act’).

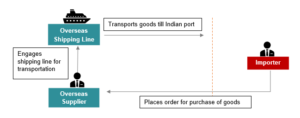

Before discussing the judgment in detail, let us understand the transaction on which the judgment was pronounced:

Section 5(3) of the IGST Act empowers Central Government to notify services on which the recipient shall be liable to pay tax. S.No.9(ii) of Notification No.8/2017-Integrated Tax (Rate) (Services Rate Notification) prescribes rate of GST on services provided by overseas shipping line to overseas supplier. Further, S.No.10 of Notification No.10/2017-Integrated Tax (Rate) (‘Reverse Charge Notification’) places the liability to pay tax in such a case upon the importer of goods.

In case of CIF imports, the service of transportation of goods is provided by overseas shipping line to overseas supplier. The importer is neither the supplier nor the recipient of the service. Hence, the importer cannot be made liable to pay GST under Section 5(3) of the IGST Act.

The High Court acknowledged this vacuum in law and struck down the levy on the following grounds:

|

S.No. |

Ground |

Judgment |

|

1. |

Importer of goods is not the recipient of service |

|

|

2. |

Transaction does not attract levy under the GST law

|

|

|

3. |

Notifications are contrary to Article 265 of the Constitution of India

|

|

|

4. |

No provision to determine time and value of supply

|

|

|

5. |

ITC is available only to recipient of supply

|

|

|

6. |

No provision for reporting in GST returns

|

|

|

7. |

Dual levy is against the settled principles of law

|

|

Basis above, the Court declared both Services Rate Notification and Revere Charge Notification as unconstitutional and ultra-vires the GST law.

NITYA Comments

This is a landmark and a well-reasoned judgment on various counts. However, the issue will be finally settled by the Supreme Court.

The Government is likely to bring retrospective amendment in the GST laws to effectuate this levy and overrule the above judgment.

In our view, a taxpayer can still challenge the levy of GST basis the Gujarat High Court judgment in the case of Sal Steel Limited v. Union of India, 2020-TIOL-163-HC-AHM-ST wherein the Court struck down the levy of Service Tax on identical transaction. One of the grounds adopted by the Court in this case is that in scheme of Service Tax law, levy can only be imposed either on the supplier or the recipient. A third person having no connection with a transaction taking place outside India, cannot be asked to pay tax.

Taxpayers engaged in taxable business, can continue to pay tax on this transaction and avail ITC to avoid any litigation in future. Taxpayers engaged in exempt business (who are unable to avail full ITC) or having ITC accumulation, can choose to litigate the issue by filing writ petition in jurisdictional High Courts.

0 Comments